by Robert Romano

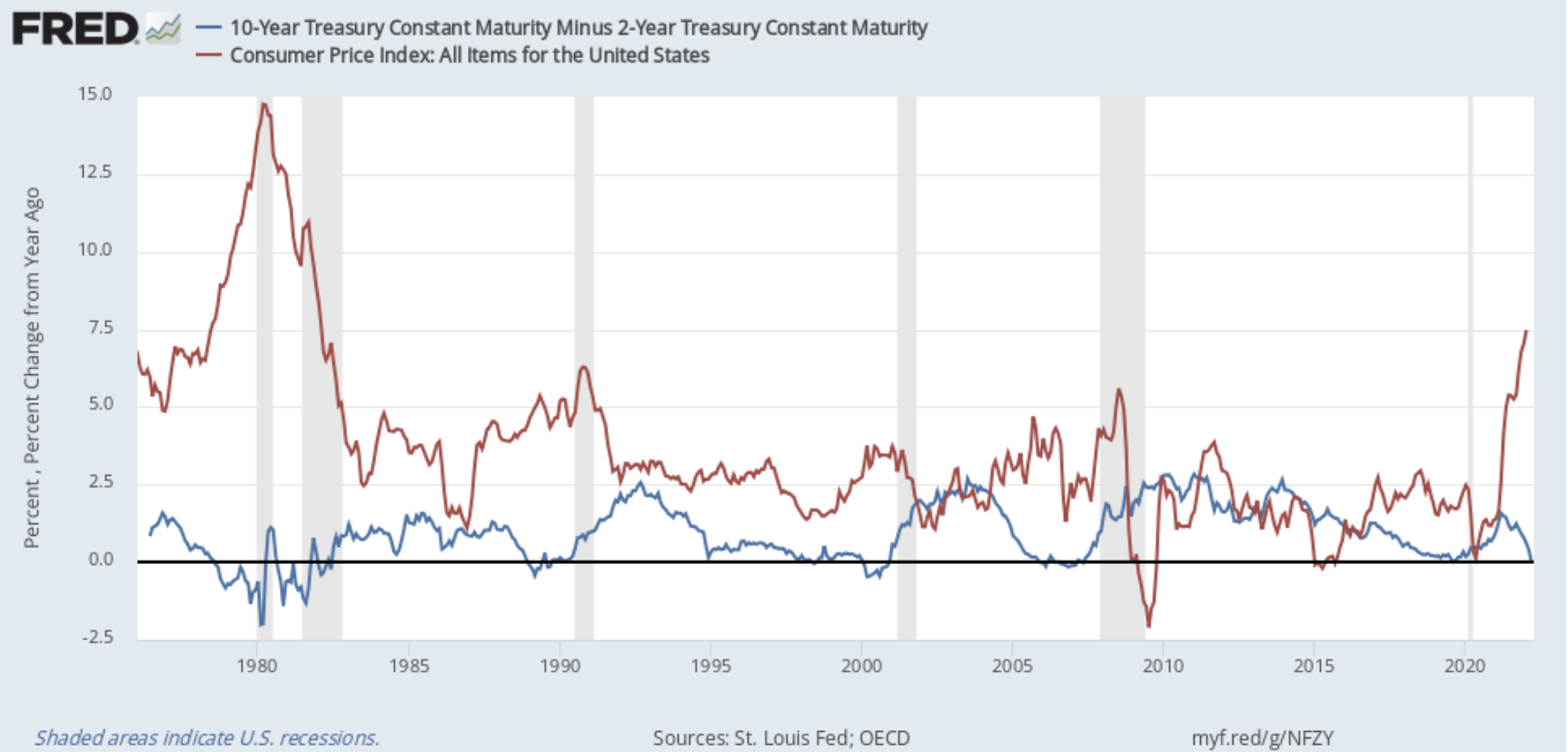

The spread between 10-year treasuries and 2-year treasuries, a leading recession indicator whose inversions have predicted almost all of the U.S. economic recessions in modern history, on March 31 inverted for the first time since Sept. 2019.

When the 10-year, 2-year spread inverts, a recession tends to result on average 14 months afterward, sometimes sooner, sometimes later. The one time there was a head fake on the 10-year, 2-year was in the mid-1990s at a time when inflation was much lower Visit Site than it is now.

As an aside, potentially the Sept. 2019 inversion might have ended up being a premature indicator, too, but then Covid and global economic lockdowns in early 2020 went ahead and ensured a recession even if one was not due. On the other hand, at that point it had been 11 years since the prior recession and so the business cycle was going to end sooner or later.

In this case, with 7.9 percent consumer inflation and 10 percent producer inflation, plus peak employment, the economy is almost certainly overheating. In fact, in modern economic history, when inflation gets above 5 percent, similar to the 10-year, 2-year, a recession tends to follow on average 14 months later. And inflation has been above 5 percent since June 2021.

Which, by the way, is no surprise.

Congress spent and borrowed more than $6 trillion to fight Covid after Jan. 2020: the $2.2 trillion CARES Act and the $900 billion phase four legislation under former President Donald Trump, and the $1.9 trillion stimulus and $550 billion of new infrastructure spending under President Joe Biden.

As a result, the national debt has increased by $6.8 trillion to $30 trillion since Jan. 2020, of which the Fed monetized half, or $3.4 trillion, by increasing its share of U.S. treasuries to a record $5.7 trillion while the M2 money supply has increased by $6.4 trillion to $21.8 trillion, a 42 percent increase, since Jan. 2020.

Throw in the supply chain crisis — production slowed down significantly in 2020 but then recovered sooner than expected, leading to supply strains in everything from oil and gas to semiconductors — and the war in Ukraine and consequent sanctions that have made the global economy that much smaller by restricting supplies further.

It is Milton Friedman’s “too much money, chasing too few goods.”

Particularly, the $1.9 stimulus in 2021 looms large as an additional catalyst for the current bout of high inflation. It was unneeded. 16 million out of the 25 million jobs lost to Covid had already been recovered before Biden was even sworn into office. The recovery was already well underway. It was an unforced error. He could have passed legislation that did a lot of things instead he opted for more helicopter money checks and child tax credits, and as a result inflation has been above 5 percent since June 2021.

Another confirming indicator could be the Job Openings and Labor Turnover Survey by the Bureau of Labor Statistics, which shows that the number of job openings has dropped for two consecutive months by almost 200,000 jobs. Usually, at the end of the business cycle, the amount of job openings first peaks and then months later declines when the recession strikes. Certainly something else to be watchful of.

Finally, there’s the Federal Reserve, which has belatedly begun hiking interest rates in March. Usually, the Fed starts to raise interest rates towards the end of the business cycle, mostly so it has room to maneuver when the next recession strikes.

For Biden’s sake, he better hope that if there is a recession, it happens before the midterms so the American people get their discontent out of their system in November and not in 2024. If not, a 2023 or 2024 recession could be putting the final nails in the coffin of another one-term presidency. Stay tuned.

– – –

Robert Romano is the Vice President of Public Policy at Americans for Limited Government Foundation.